Tareno View January 2026

Published: 13.01.2026

Growth remains, favorites rotate

The global economy has also proven to be remarkably resilient in 2025. Despite all the prophecies of doom, the global economy is growing steadily, driven by a powerful triad of expansive fiscal policy, looser monetary policy and technological progress. This has been a blessing for investors: Equity markets and mixed mandates once again delivered pleasing returns. However, past success is no guarantee for the future. As the economy gains momentum and growth broadens, opportunities are shifting away from the celebrated winners of recent years towards neglected segments. In this issue, we shed light on why active selection will be crucial in 2026 and how portfolios can be set up to be robust and generate strong returns in different scenarios.

Macroeconomic environment: fuel for the global economy

Although the geopolitical and economic policy shifts emanating from the USA in 2025 kept the world on tenterhooks, they hardly left a mark on the hard currency of global growth. Adjusted for inflation, the global economy grew by a solid 3%, as in previous years. For the current year, the signs are not only pointing to a continuation, but to an acceleration. Three powerful forces are working in unison here:

Expansionary fiscal policy as a permanent condition

Government spending remains at an exceptionally high level globally. In the USA, tax breaks and industrial policy are causing a deficit of around 8%. At the same time, deregulation and a leaner state apparatus should mobilize private investment and free up productivity. Europe is following with a time lag, but with increasing determination. The German investment program in particular is now taking effect and providing impetus in the areas of armaments, energy and infrastructure. China completes the picture as the third major player. With a deficit also close to 8%, Beijing is stabilizing the domestic economy and counteracting deflationary tendencies. Taken together, these fiscal forces form a robust foundation for sustained global growth of around 3%.

Monetary policy under fiscal pressure

In view of this major fiscal situation, a restrictive monetary policy would traditionally be appropriate in order to avoid overheating. However, the reality of high debt levels dictates a different logic: central banks are under pressure to keep financing costs low. Even though the majority of interest rate cuts may be behind us, the compass of most central banks continues to point in the direction of easing. In addition to cutting interest rates, the US Federal Reserve recently switched from withdrawing liquidity to injecting it. Monetary policy is thus once again becoming an ally of growth and the capital markets.

Technology as a productivity turbo

Around a third of US growth in the past year is directly attributable to investments in AI infrastructure. Even higher budgets are available for 2026, and industry experts are forecasting a multiplication of computing capacities in the coming years. However, the decisive factor is when these investments will pay off. We are seeing companies successfully integrating AI in more and more sectors. Productivity gains are already measurable, particularly in software development, industrial automation and biotechnology. 2026 is likely to be the year in which these effects are broadly reflected in company profits and overall economic productivity for the first time.

Market commentary: The renaissance of market breadth

In 2025, the world equity index recorded double-digit growth for the third year in a row. Encouragingly, mixed mandates also enjoyed above-average gains. The relative strength of Europe compared to the USA, reinforced by the depreciation of the US dollar, was remarkable.

After three strong years, the question arises as to the sustainability of this trend. A look at the two drivers of the stock markets, earnings growth and valuation, makes us confident, but at the same time warns us to take a differentiated view.

Profit growth: From a few to many

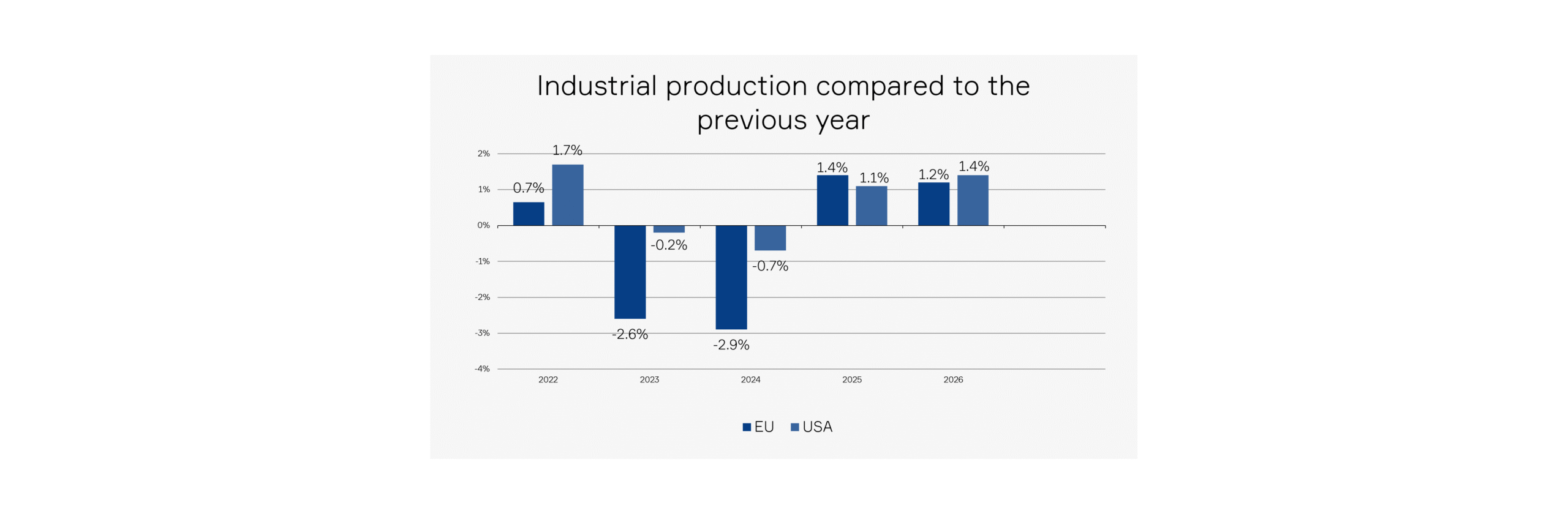

The favorable macroeconomic environment forms the breeding ground for solid profit growth. The key difference compared to previous years lies in the distribution: whereas recently it was almost exclusively technology giants that were responsible for the profit increases, we now expect a significant broadening. Cyclical sectors are benefiting from investment programs, more stable supply chains and lower interest rates. Industrial production is expanding again in the US and the EU after two years of contraction.

Reviews: Deceptive index view

A look at the major indices shows historically high valuations, which call for caution. Historically, such levels have led to below-average returns over longer periods of time. However, this view falls short of the mark. Away from the major indices, there are numerous market segments with moderate to attractive valuations. For active investors, this opens up the possibility of achieving better returns in the coming years with a broadly diversified equity portfolio than purely index-oriented strategies. Two areas appear particularly attractive to us:

Firstly, defensive sectors such as healthcare and consumer staples. There is a large valuation gap between these and the cyclical sectors and technology. Medical technology in particular offers structural growth at attractive valuations.

Secondly, small and mid caps offer a significant valuation discount compared to large caps. The combination of industrial recovery and lower key interest rates favors these smaller companies disproportionately. This is reflected, for example, in our water fund, whose valuation has fallen to attractive levels over the past year.

Investment policy: Flexibility as a constant

The repeated, sometimes abrupt changes in the investment environment in recent years have shown that a forward-looking and flexible allocation can create real added value. We see three virtues as central to successful implementation:

Discipline instead of greed

Markets tend to exaggerate in the short term, especially when temporary profit trends are projected linearly into eternity. We remember the euphoria surrounding vaccine stocks or home office profiteers. After strong price gains and signs of overheating, it is advisable to take profits and reallocate capital to structurally intact but undervalued segments. We currently consider profit-taking in the technology and financial sectors to be appropriate. At the same time, we see attractive return potential in quality stocks outside the market favorites, in defensive sectors and in second-line stocks.

Genuine, active diversification

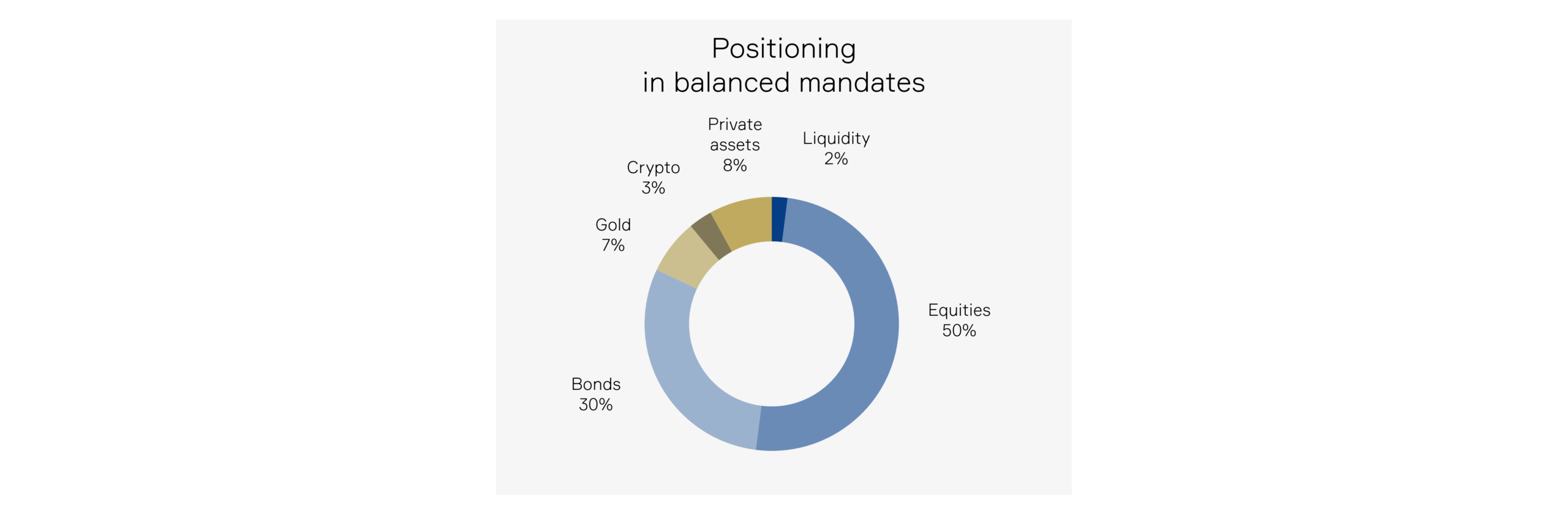

Index funds often convey a deceptive sense of diversification. In fact, investors are taking considerable cluster risks. True diversification requires an ongoing review and adjustment of the allocation. The addition of new asset classes such as private market investments and cryptocurrencies increases the robustness and return potential of portfolios. At equity level, we recommend that index-tracking investors reduce their heavy weighting in the US and technology and selectively reallocate to underrepresented sectors and regions, such as the healthcare sector and emerging markets.

Taking risks seriously, protecting assets

Forecasts are naturally subject to uncertainty. In addition to our positive base scenario, we must prepare for alternative outcomes. We see the greatest risk in a return of inflation, which monetary policy can only counteract to a limited extent in view of the immense national debt. The danger of a creeping devaluation of money is real. In terms of wealth preservation, we recommend a clear focus on real assets (equities, real estate and commodities) and the deliberate inclusion of alternative investments. They increase the resilience of the portfolio across different scenarios and form a central return component of our portfolios.

Imprint

Tareno AG, Gartenstrasse 56, CH-4052 Basel, +41 61 282 28 00

Tareno AG, Claridenstrasse 34, CH-8002 Zurich, +41 44 283 28 00

info@tareno.ch

www.tareno.ch

Responsible

Simon Lutz

Chief Investment Officer

s.lutz@tareno.ch

Disclaimer

The statements and information in this publication have been compiled by Tareno AG to the best of its knowledge, in part from external (publicly accessible) sources which Tareno AG considers to be reliable, for information purposes only. This publication is not the result of a financial analysis. Tareno AG and its employees are not liable for incorrect or incomplete information or for losses or lost profits resulting from the use of information and the consideration of opinions expressed. The statements and information do not constitute a solicitation or invitation, offer or recommendation to buy or sell any investment instruments or to engage in any other transactions.

Nor do they constitute a specific investment proposal or other advice on legal, tax or other issues. A positive return on an investment in the past is no guarantee of a positive return in the future. The statements, information and opinions expressed herein are current only as of the date of this document and are subject to change at any time.

Duplication or reproduction of this publication, even in part, is not permitted without the written consent of Tareno AG. The “Guidelines for Ensuring the Independence of Financial Research” of the Swiss Bankers Association do not apply.

Images: Marijke Vosmeer, IStock, Pixabay, Unsplash, Lucia Hunziker

Charts: Tareno AG