Tareno Healthcare Funds: Monthly report February 2026

Market overview

M&A activity remained robust, with the largest biotech and medtech deals so far this year. Gilead Sciences acquired Arcellx for USD 7.8 billion. In the MedTech sector, Danaher agreed to pay USD 9.9 billion for pulse oximeter manufacturer Masimo.

The reporting season is largely over. The Q4-2025 results showed a mixed picture. More than two thirds of companies exceeded EPS expectations, albeit with a smaller positive deviation than in the previous year. The sales trend was somewhat stronger: a higher proportion of companies exceeded sales estimates and the average positive deviation was also slightly higher year-on-year.

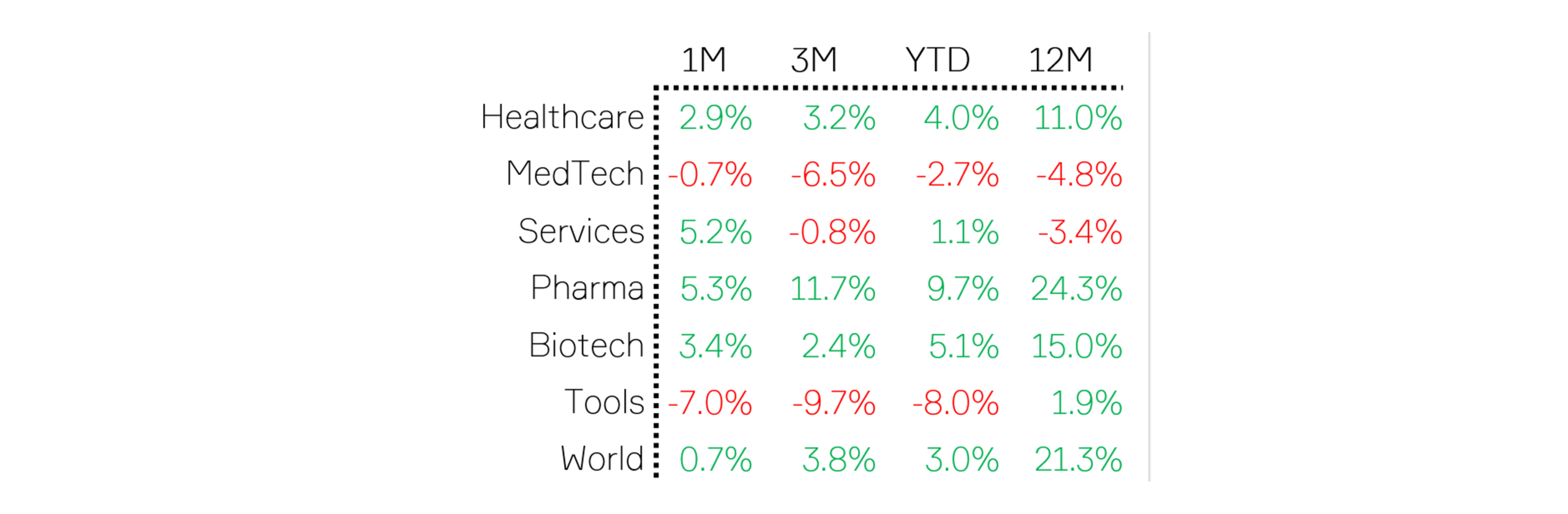

Pharma again led performance in February, underlining its defensive profile and relative insulation from macroeconomic (and AI-related) volatility. Obesity remained the dominant theme. Novo Nordisk’s CagriSema failed to demonstrate non-inferiority to the high-dose version of Eli Lilly’s Zepbound. This calls combination therapies into question and further strengthens Lilly’s positioning in the GLP-1 market. The data for Pfizer/Metsera’s lead obesity candidate was mixed: Although placebo-adjusted weight loss was higher than that of semaglutide, it was lower than that of tirzepatide. Competitive fears increased after Hims & Hers attempted to launch a compounded semaglutide pill, triggering a swift response from the FDA. Fears around copycat products meanwhile caused Novo Nordisk and Eli Lilly to lose over USD 95 billion in combined market capitalization before FDA Commissioner Marty Makary announced swift action against illegal copycat drugs.

Providers & Services developed almost in step with Pharma, driven by strength among drug distributors, hospitals and domestic laboratory service providers.

Biotechnology ended the month in positive territory, but showed significant volatility – reflecting its continued sensitivity to regulatory headlines and the broader macro environment. On a positive note, several IPOs were launched on the market.

Life Science Tools & Services was the weakest sub-sector. Fears of AI disruption weighed heavily on CROs in particular. A report on AI-driven risks to traditional clinical trial and contract research models weighed on sentiment. In addition, company-specific developments exacerbated the weakness, including the delay in the presentation of ICON’s figures, the withdrawal of guidance and the disclosure of an investigation by the Audit Committee into accounting practices. Regulatory issues also remained in focus, with the FDA introducing a new one-study approval pathway to replace the previous two-study requirement. This initially put pressure on shares, although sentiment later improved as simplified studies could increase outsourcing demand in the long term.

Overall, there was a clear dispersion between the healthcare subsectors in February. Pharma maintained its defensive “safe-haven” characteristics, while Life Science Tools & Services fluctuated sharply due to AI disruption fears – in our view to some extent excessively.

The chart shows the development of all sectors in the past year:

Source: Tareno AG

Portfolio Tareno Sustainable Healthcare Fund

Last month, we built up a position in Johnson & Johnson and did not sell any existing positions. In February, the Tareno Sustainable Healthcare Fund generated a return of 0.7%, while the benchmark index rose by 2.9%.

The biggest positive attribution drivers compared to the index were:

- AstraZeneca (+26 bps): Solid Q4 numbers driven by Oncology and a strong 2026 outlook, with a broad Phase III data calendar for 2026-27 underpinning confidence in the pipeline. The stock also benefited from mixed Phase 2 asthma data from Upstream Bio and general pharma strength in February.

- Merck & Co(+24 bps): Share price up after solid Q4 results despite mixed (and largely anticipated) guidance for 2026. Again, general pharma strength supported.

- Novartis (+16 bps): Share price gains after solid Q4 figures, adjusted for one-off US discount effects (Kisqali, Entresto). Cosentyx and Pluvicto were above expectations. General pharma strength.

The biggest negative attribution drivers in relation to the index were:

- Novo Nordisk (-82 bps): Forecast for declining sales and EBIT in 2026 due to US pricing pressure and increasing competition in the obesity market. Additional pressure from Hims & Hers Health’s announcement of a low-cost semaglutide pill (later banned by the FDA). The REDEFINE-4 study also failed to meet the primary endpoint of non-inferiority to tirzepatide.

- Boston Scientific (-40 bps): Q4 above expectations, but with different sales mix (Electrophysiology, Watchman); guidance slightly below expectations.

- Johnson & Johnson (-40 bps): The stock rose 10%; we are underweight the index.

Portfolio Review Tareno Impact Healthcare Fund

Last month we built up a position in Guardant Health and sold Exact. In February, the Tareno Impact Healthcare Fund generated a return of -1.6%.

The biggest positive contributions were:

- Aspen Pharmacare (+92 bps): Positive trading update.

- Tandem Diabetes Care (+82 bps): Solid Q4 figures; the switch to a “pay-as-you-go” model was positively received by the market.

- sandoz (+41 bps): Benefited from a broker upgrade and later solid Q4 numbers (revenue in line, EPS above expectations) with better guidance for 2026.

The biggest negative contributions were:

- Novo Nordisk (-143 bps): Forecast for declining sales and EBIT in 2026 due to US pricing pressure and increasing competition in the obesity market. Additional pressure from Hims & Hers Health’s announcement of a low-cost semaglutide pill (later banned by the FDA). The REDEFINE-4 study also failed to meet the primary endpoint of non-inferiority to tirzepatide.

- Hikma (-53 bps): H2 figures above expectations, but 2026 guidance below consensus. Withdrawal of medium-term guidance following strategic review by new CEO and several management changes.

- Axsome (-45 bps): Q4 figures communicated in advance; share price down due to investor concerns about increased costs due to expansion of sales team.

Would you like to find out more?

Do you have any questions about the monthly report or the Tareno Healthcare Funds? We look forward to hearing from you.

Publications

Tareno Healthcare Fund

Disclaimer

This document has been prepared for marketing and informational purposes only and does not constitute an offer or a solicitation to subscribe for, purchase, or sell units of this investment fund. It does not constitute investment advice. Only the current fund documents (in particular the prospectus and the Key Information Document (KID)) are legally binding. Past performance is not a reliable indicator of future results. Images: Marijke Vosmeer, Luzia Hunziker, Jürg Kaufmann, iStock, Unsplash / Graphics: Tareno AG, Bloomberg