Tareno View April 2026

Published: 14.04.2026

With calm and discipline through geopolitical uncertainty

The third Gulf War has been keeping the financial markets on tenterhooks for a good six weeks now. New, sometimes contradictory signals from Washington on a daily basis are forcing investors to constantly reassess the situation. The focus is on three questions: How long will the Strait of Hormuz remain blocked? How will energy prices develop? And what does the supply shock mean for inflation, interest rates and growth?

Especially in such an environment, it is crucial to see through the geopolitical uncertainty with calm and discipline and to maintain a comprehensive, longer-term view. In this Tareno View, we explain how we assess the macroeconomic situation, where we see opportunities and risks on the markets and how we position our portfolios in this uncertain environment. Our quintessence beforehand: stick to the investment strategy, but exercise caution with new risk investments following the sharp price recovery.

Macroeconomic environment

Limited energy price shock

Since the outbreak of the war, the debate has revolved around its macroeconomic consequences. One thing is clear: a blocked Strait of Hormuz will lead to a severe shortage of energy and other raw materials from the Persian Gulf. The economic chain reaction includes higher energy prices, rising inflationary pressure, tighter interest rate expectations and lower growth forecasts. Accordingly, the capital markets have come under pressure in the short term.

However, it is not the shock itself that is decisive, but its duration. The longer the trade route remains blocked and the more the energy infrastructure is damaged, the greater the risk that a temporary supply shock will result in a broader, negative economic and inflationary impulse. A ceasefire has been in place since April 8. Diplomatic talks have so far been inconclusive, but an agreement in the coming weeks seems realistic, as the costs of further escalation would be considerable for both sides.

Structural growth forces remain intact

Our base scenario therefore remains that the Strait of Hormuz will not be closed for an extended period and energy prices will not continue to rise significantly. In this case, global inflation rates are likely to rise only moderately temporarily, which would not force the major central banks to raise interest rates again, meaning that the positive economic momentum should continue, supported by two important structural growth drivers:

Firstly, artificial intelligence continues to drive a massive investment cycle in data centers and energy infrastructure. Secondly, fiscal policy in the US, Germany and Japan is having an expansionary effect. As long as the energy shock remains limited in time, we therefore do not see a break in the global growth path, but rather a temporary burden within an economic environment that remains robust.

This is also evidenced by a large number of high-frequency economic indicators, such as the Dallas Fed’s Weekly Economic Index, which provides a timely signal of current real economic activity in the US on the basis of several daily and weekly data series and is scaled to GDP growth. The most recent value from April 9 signals above-average growth of 2.7%.

Market commentary

The markets are focusing on normalization

With the ceasefire, the global stock markets have clearly recovered from their lows and are now trading only moderately below their highs.

The sigh of relief on the stock markets is understandable, but it would be premature to sound the all-clear. If the negotiations fail or there are renewed attacks on energy infrastructure and transport routes, the consequences would be much more serious than in our baseline scenario. A prolonged supply shock would not only fuel inflation, but also put pressure on the profit margins of energy-intensive companies and put central banks in an unpleasant dilemma.

The risks are only priced in to a limited extent

This is precisely why we urge caution when making new investments. Investor sentiment has already returned to neutral territory and the futures markets for crude oil are once again anticipating a significant fall in oil prices. In other words, the risks are only reflected in prices to a limited extent. If there is a renewed escalation, there is potential for disappointment.

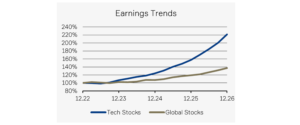

Technology is more attractive again

Apart from the conflict in the Middle East, the large performance discrepancy between the sectors on the stock market is striking. Following the weak phase of technology stocks, we are revising our more cautious stance from the beginning of the year. While share prices corrected, earnings estimates were adjusted further upwards.

This has largely reduced the valuation premium of the technology sector compared to the market as a whole. In our view, above-average growth at reasonable valuations again forms an attractive basis for future returns in the technology sector.

Investment policy

Focused on growth, armed against inflation

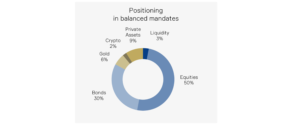

Since the beginning of the war, we have advised investors to remain true to their investment strategy and to avoid panic selling. This assessment has so far proven to be correct and remains valid. Based on the robust economic momentum, our focus remains clearly on equities, supplemented by investments with inherent inflation protection. For us, these include infrastructure investments, gold and cryptocurrencies in particular. They fulfill different functions, but together they increase the robustness of the portfolio in an environment characterized by inflation risks.

Anticyclical between euphoria and fear

In the first quarter, we realized some of the gains on our gold position near the highs and at the same time increased our Ethereum position by around 20% below current levels. The sentiment in both segments could hardly have been more contrasting. Following the sharp rise in the price of gold, there were increasing signs of euphoria. In the crypto sector, on the other hand, sentiment indicators signaled extreme fear, although little had changed in the fundamental picture. It is precisely in such phases that the value of a disciplined, anti-cyclical approach becomes apparent.

USD risks remain in the medium term

We see the US dollar stabilizing in the short term, but no structural change of direction. The conflict has temporarily supported the dollar, buoyed by higher US yields and inflows into safe havens. However, as geopolitical stress eases, the overarching downtrend is likely to come to the fore again. It therefore remains sensible for CHF and EUR investors to hedge some of their USD risk.

Bonds are becoming somewhat more interesting again

Although bonds are not one of our preferred asset classes, the picture has improved. With the war, yield curves and credit spreads have shifted upwards. As a result, bonds are significantly less unattractive than they were at the beginning of the year. With maturities and surplus liquidity, opportunities are opening up again in the medium maturity range.

Imprint

Tareno AG, Gartenstrasse 56, CH-4052 Basel, +41 61 282 28 00

Tareno AG, Claridenstrasse 34, CH-8002 Zurich, +41 44 283 28 00

info@tareno.ch

www.tareno.ch

Responsible

Simon Lutz

Chief Investment Officer

s.lutz@tareno.ch

Disclaimer

The statements and information in this publication have been compiled by Tareno AG to the best of its knowledge, in part from external (publicly accessible) sources which Tareno AG considers to be reliable, for information purposes only. This publication is not the result of a financial analysis. Tareno AG and its employees are not liable for incorrect or incomplete information or for losses or lost profits resulting from the use of information and the consideration of opinions expressed. The statements and information do not constitute a solicitation or invitation, offer or recommendation to buy or sell any investment instruments or to engage in any other transactions.

Nor do they constitute a specific investment proposal or other advice on legal, tax or other issues. A positive return on an investment in the past is no guarantee of a positive return in the future. The statements, information and opinions expressed herein are current only as of the date of this document and are subject to change at any time.

Duplication or reproduction of this publication, even in part, is not permitted without the written consent of Tareno AG. The “Guidelines for Ensuring the Independence of Financial Research” of the Swiss Bankers Association do not apply.

Images: Marijke Vosmeer, IStock, Pixabay, Unsplash, Lucia Hunziker

Charts: Tareno AG