Tareno View July 2025

published: 09.07.2025

With future-oriented allocation to investment success

The second quarter of 2025 has once again shown investors how quickly economic and political conditions can change and how crucial careful asset allocation is. Despite initial uncertainties caused by renewed US tariff discussions, global markets proved remarkably resilient and quickly reached new highs.

This development confirms our belief in a balanced, forward-looking and dynamic asset allocation. Especially in a world characterized by political uncertainties and rapid technological changes, a strategy that is broadly diversified and at the same time able to react flexibly to market developments pays off. With our latest investment in the innovative and agile “Hawk-Eye” equity strategy, we are now taking even greater account of this investment policy.

Macroeconomic environment

US government reaches its limits

The US tariff theater may seem unnecessary and tiresome, but it also has positive side effects: Governments, companies and investors are increasingly questioning their cluster risks and economic dependencies. This is giving Europe additional impetus for overdue structural reforms. At the same time, the economy and financial markets are once again demonstrating their resilience and corrective power in the face of misguided policies. The US government had to quickly realize that global supply chains cannot be restructured in the short term and that irresponsible financial policies are immediately punished by higher borrowing costs.

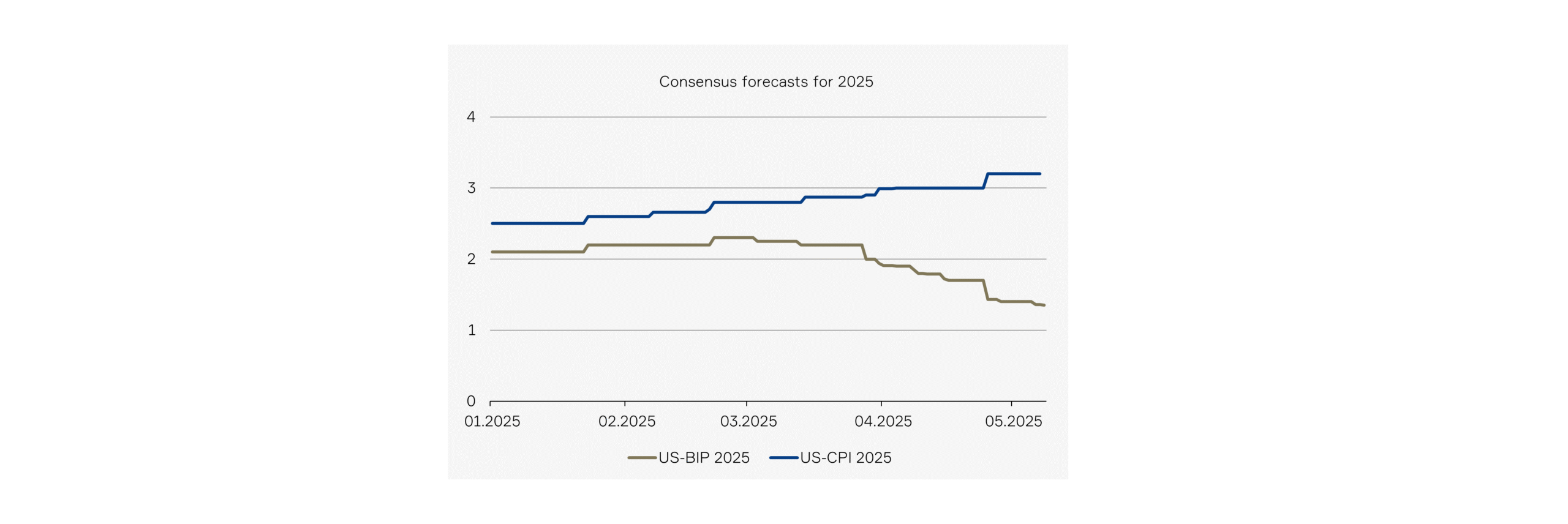

It is therefore not surprising that the US President had to quickly withdraw the announced “reciprocal” tariffs. The effective US tariff rate was reduced from the originally announced 25% to around 15%, consisting of basic tariffs for all countries and special tariffs for China and selected industries. We expect tariffs to stabilize at this level. This should have a negative but limited impact on the economy, which is also reflected in the forecasts for 2025.

Ironically, the trade restrictions are weighing most heavily on the US economy: growth is likely to fall by around 1%, while inflationary pressure is rising again. The real impact is likely to become apparent in the coming months once companies have reduced their precautionary import inventories.

Market commentary

Strong markets despite tariffs

The brief tariff shock at the beginning of April only unsettled the financial markets for a short time. Just one month later, the markets had fully recovered and are currently at new highs. The resilience of the stock markets is well founded, as fundamental drivers such as corporate profits are proving to be robust.

Despite the customs problems, profit growth is expected in all key regions over the next 12 months (USA +7%, Europe +1%, Switzerland +9%, emerging markets +14%). The earnings performance of recent years shows impressively how well companies can deal with uncertainties.

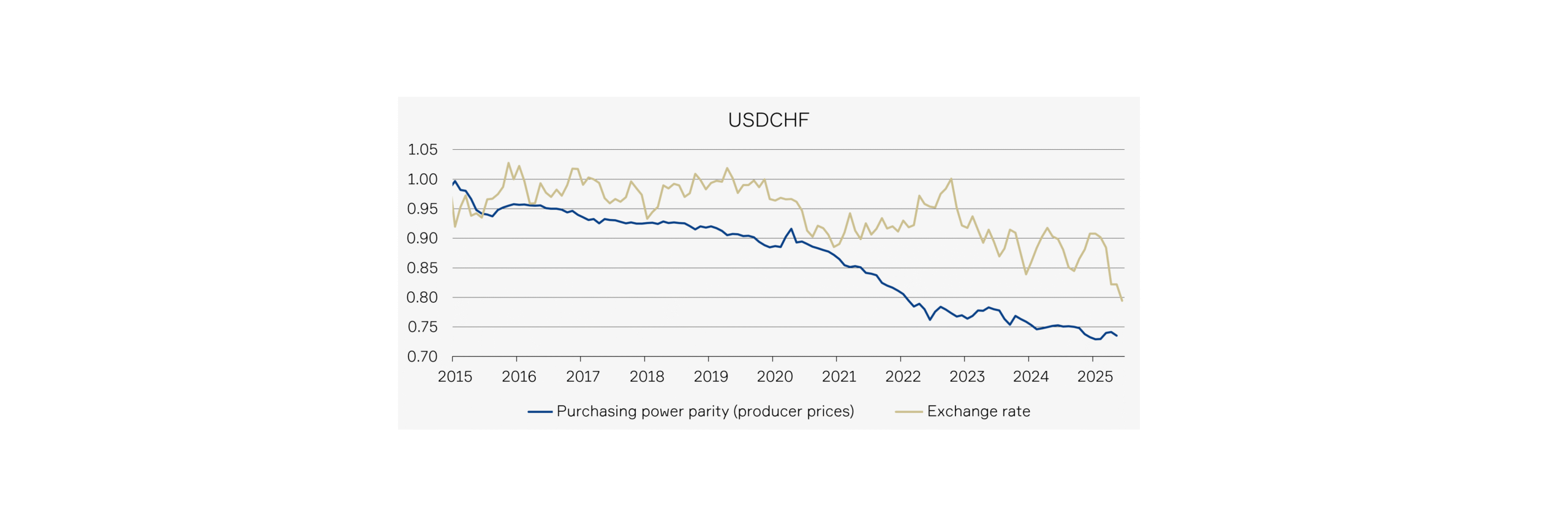

From the perspective of CHF and EUR investors, however, this positive development is clearly put into perspective, as the US dollar has depreciated by 12% against these currencies since the beginning of the year.

This significant devaluation comes as no surprise: the USD was clearly overvalued at the start of the year, supported by capital inflows due to attractive yields. All that was missing was a catalyst, and that was the unpredictable US policy. This caused the dollar to lose its shine and confidence. The role of the US dollar as the backbone of the global financial system is increasingly being called into question. However, there is currently no viable alternative in sight. Nevertheless, global investors and governments will try to reduce their dependence. In the medium term, we therefore expect the US dollar to weaken further towards purchasing power parity.

From a short-term perspective, however, we believe that the weakness of the USD is exaggerated. In combination with the high hedging costs of currently 4.5% p.a., we have therefore reduced our currency hedging ratio in the CHF portfolios from 50% to 40%.

Investment policy

Taking asset allocation further

The political surprises and divergent market developments in the first half of 2025 once again reinforce our investment policy, which is based on a balanced, forward-looking and dynamic asset allocation.

Balanced.

Many investors focus too heavily on sub-optimal indices and thus unintentionally take on high cluster risks. For example, the world stock index is US and technology-heavy, while the Swiss index is heavily dominated by a few stocks and lacks sectors such as technology, commodities and energy. Efficient risk management, on the other hand, requires genuine diversification across currencies, regions, sectors, investment styles and asset classes.

Forward-looking.

The asset management industry has traditionally based its strategic allocation primarily on historical return and risk metrics. The disadvantage of this approach is that investments focus mainly on the winners of the past and important changes and trends in the investment world are often overlooked. For example, it can be observed that portfolios are unintentionally increasingly geared towards the US currency after a prolonged period of USD appreciation or continue to be invested in CHF bonds, even though these hardly generate any income with negative interest rates.

A forward-looking and successful asset allocation, on the other hand, is based on forecast returns and risks. Although these key figures cannot be observed directly and must be carefully estimated, it is precisely this sophisticated approach that promises the decisive added value. Only with such a forward-looking strategy can investors invest early in new asset classes such as Bitcoin and emerging sectors such as cyber security.

Dynamic.

Financial markets are prone to exaggerations and regime changes that require portfolio adjustments. A purely static allocation would therefore be too inflexible and inefficient. At the same time, frequent tactical reallocations in anticipation of short-term market movements are usually not very promising and often result in high costs with manageable or even negative returns. Our approach is therefore deliberately dynamic with a medium-term horizon of several years. In practice, this means that we react anti-cyclically to short-term exaggerations, identify new technologies and long-term economic changes and continuously and carefully adjust the allocation to the investment environment. As the focus of the financial markets can quickly shift from one topic to another, agility is also required. We have recently increased this further by adding our “Hawk-Eye” to our portfolios. This innovative equity strategy has been very successfully identifying global trends and the winners of tomorrow since the beginning of 2023.

Imprint

Tareno AG, Gartenstrasse 56, CH-4052 Basel, +41 61 282 28 00

Tareno AG, Claridenstrasse 34, CH-8002 Zürich, +41 44 283 28 00

info@tareno.ch

www.tareno.ch

Disclaimer

The statements and information in this publication have been compiled by Tareno AG to the best of its knowledge, in part from external (publicly accessible) sources which Tareno AG considers to be reliable, for information purposes only. This publication is not the result of a financial analysis. Tareno AG and its employees are not liable for incorrect or incomplete information or for losses or lost profits resulting from the use of information and the consideration of opinions expressed. The statements and information do not constitute a solicitation or invitation, offer or recommendation to buy or sell any investment instruments or to engage in any other transactions.

Nor do they constitute a specific investment proposal or other advice on legal, tax or other issues. A positive return on an investment in the past is no guarantee of a positive return in the future. The statements, information and opinions expressed herein are current only as of the date of this document and are subject to change at any time.

Duplication or reproduction of this publication, even in part, is not permitted without the written consent of Tareno AG. The “Guidelines to ensure the independence of financial analysis” of the Swiss Bankers Association do not apply.

Images: Marijke Vosmeer, IStock, Pixabay, Unsplash, Lucia Hunziker

Charts: Tareno AG