Brunetti View December 2025

Published: December 16, 2025

One year of Maga-Economics

It is probably the biggest experiment in unconventional economic policy that we have seen in a rich industrialized country in recent decades. And it is certainly the outstanding macroeconomic event of this year. With the aim of leading the economy – subito – to unprecedented heights, hardly a single economic policy stone was left unturned in the USA this year. In the opinion of most economists, however, the methods and instruments used were highly unsuitable. Although the policy mix was actually aimed at achieving large growth gains as quickly as possible, the US economy remains remarkably undynamic. As we discussed in the last “View”, the populist expansion strategy was thwarted by the massive uncertainty created by the practically daily policy changes. As a result, the unusual policy mix has weakened growth practically from the outset. If this policy is maintained, the medium-term growth momentum of the US economy is also likely to be substantially impaired.

Customs duties as the main actor

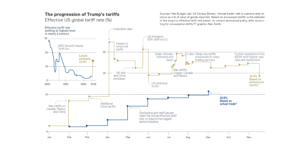

One policy area obviously stands out, namely trade policy. Tariffs are, so to speak, the symbol of Trump’s economic policy and he already emphasized during the election campaign how central he considers significant tariff increases to be. And whatever you think of it, the administration has delivered what was promised in this respect. The chart in the Financial Times, which is updated regularly, shows the impressive progression of US trade policy since the new administration took office. The small graph in the top section of the picture traces the course of average US tariffs since the beginning of the 20th century. In response to the high costs of the unfortunate protectionist measures in the interwar period (symbolized by the Smoot-Hawley Tariff Act), there was a clear rethink after the end of the Second World War. As part of the reorganization of global economic institutions, the USA took the lead in the joint efforts of industrialized countries to dismantle trade barriers as far as possible. Average tariffs were therefore reduced step by step and reached a very low level of almost zero percent in this millennium. Donald Trump brought this wave of liberalization in global trade to an abrupt end this year. Tariffs quickly shot back up to the level at the end of the Second World War. The large chart in the figure traces this spectacular development in the current year in more detail. After some initial tariff increases in the first quarter, the shock of the – originally titled – Liberation Day came at the beginning of April. From this high point, tariffs have since been reduced somewhat with some back and forth, but are currently still at a very high average of just under 15%. Incidentally, the most recent event here is the so-called “customs deal” with Switzerland.

This development is also remarkable because such a protectionist trade policy is diametrically opposed to the basic recommendations of economics. Economists debate many things, but when it comes to the harmful effects of tariffs, there is a remarkable consensus of opinion.

There are various arguments for this, but the basic reasoning is very simple. Firstly, the (international) division of labor is the basis of prosperity (imagine a self-sufficient Switzerland) and secondly, any trade only takes place if both parties benefit from it. The US administration’s argumentation makes it clear that it does not accept or understand these two premises. If, for example, it considers every bilateral trade deficit to be problematic and wants to bring the production of as many goods as possible back to the US, then it is de facto taking the immensely expensive and inefficient path towards self-sufficiency. And when it repeatedly insists that trade with certain countries is at the expense of the US, it believes that foreign trade is a zero-sum game and that one country’s gain is another’s loss. But this is a fundamental misunderstanding, because no one can be forced to trade and trade therefore only takes place if both sides benefit; it is a positive-sum game that increases the size of the cake overall and is therefore not about distributing an existing cake.

Against this backdrop, it is economically undisputed that imposing tariffs is harmful and that the US administration is doing itself and its country a monumental disservice if it continues to do so. The political-economic problem is that the costs of tariffs are primarily long-term. In the short term, they are attractive because they appear to protect domestic production and at the same time generate government revenue. However, the costs come mainly in the longer term because the value chains have to be reorganized and become less efficient and the workforce is deployed less productively. This significantly reduces future growth potential. However, one negative effect can already be felt in the short to medium term, namely the increase in the price of goods.

Threat of inflation (loss of purchasing power)

And this brings us to the second particularly remarkable effect of Trump’s policy mix. Practically all measures threaten to fuel inflation. The first is the trade policy just described. A large proportion of the tariffs are generally passed on to customers. It is clear to see that this has already begun in the USA, as consumers are increasingly complaining about the falling affordability of goods that are subject to high tariffs. However, the severe restrictions on migration are also leading to wage pressure and thus price increases due to the increasing shortage of labor. Budgetary policy has the same effect through tax cuts combined with continued extraordinarily high government spending. And last but not least, the administration is constantly attacking the US central bank and demanding drastic interest rate cuts. These attacks undermine the independence of the central bank, which is central to price stability, and any further interest rate cuts would also have an inflationary effect. Overall, all elements of this policy mix are driving up prices and it is therefore no surprise that US inflation, and core inflation in particular, is stubbornly holding steady at 3% despite the gloomy economic trend. Rising inflation expectations also indicate that the peak of this trend has probably not yet been reached.

… and Switzerland?

As is well known, Switzerland was hit particularly hard by the US tariff hammer. Accordingly, a slump in goods exports led to weak GDP growth in the second quarter and a significant decline in the third. As a country heavily dependent on exports, Switzerland cannot escape such a foreign trade shock. On a positive note, there are now signs of an agreement that should lead to a reduction in tariffs from a stratospheric 39% to a still high 15%. The decisive factor here is that Switzerland is likely to have a similar burden to the EU, which will reduce additional crowding-out effects to its detriment. Accordingly, a slight recovery in the outlook is to be expected and the GDP slump in the third quarter may not mean the start of a recession after all.

In general, the latest reactions from the US administration show that it is beginning to realize that tariff policies are increasing prices, reducing the affordability of goods for US households and thus increasingly affecting the government’s popularity. It is therefore quite conceivable that protectionist measures will be scaled back somewhat in the near future, which could significantly brighten the outlook for the global economy. However, in view of the US administration’s proven unsteadiness this year, this is primarily a tentative hope for the time being.

Responsible

Prof. Dr. Aymo Brunetti

Economist, Professor of Economic Policy at the University of Bern

Simon Lutz

Chief Investment Officer

s.lutz@tareno.ch

Disclaimer

The statements and information in this publication have been compiled by Tareno AG to the best of its knowledge, in part from external (publicly accessible) sources which Tareno AG considers to be reliable, for information purposes only. This publication is not the result of a financial analysis. Tareno AG and its employees are not liable for incorrect or incomplete information or for losses or lost profits resulting from the use of information and the consideration of opinions expressed. The statements and information do not constitute a solicitation or invitation, offer or recommendation to buy or sell any investment instruments or to engage in any other transactions.

Nor do they constitute a specific investment proposal or other advice on legal, tax or other issues. A positive return on an investment in the past is no guarantee of a positive return in the future. The statements, information and opinions expressed herein are current only as of the date of this document and are subject to change at any time.

Duplication or reproduction of this publication, even in part, is not permitted without the written consent of Tareno AG. The “Guidelines to ensure the independence of financial analysis” of the Swiss Bankers Association do not apply. [Pictures: Marijke Vosmeer]