What you should consider before purchasing a fund

First: Create clarity

Before you buy a fund, ask yourself these three questions:

- What is my investment goal?

- What is my investment horizon?

- How much risk am I willing and able to take?

The first step is to note down what your goal is. Are you saving for a specific purpose? Or do you want to maintain the purchasing power of your savings despite inflation? Do you want to broaden your existing portfolio or invest specifically in a particular market or trend? The answer is very individual and determines which fund is best suited to you.

Now determine your investment horizon. How long do you want to invest your capital? Do you need the capital in the short term, or are you saving for your child/grandchild/godchild or for retirement, which is still a long way off? The investment horizon is crucial for choosing the fund and the risk you can take. As a general rule, the longer your investment horizon, the more risk you can take.

Your personal risk profile is particularly important. Define for yourself how much risk you can and want to take given your investment horizon and financial situation.

Many banks and asset managers, including us at Tareno, are happy to assist you with these questions in a personal consultation.

Once you know what you want, it’s time to explore the world of funds.

Fund universe – What are funds and how do they differ?

Essentially, a fund is a financial product that pools money from many investors and invests it in various asset classes such as stocks, bonds, or real estate according to a defined strategy. A simple comparison: a fund is like a fruit basket that contains a variety of fruits, not just apples. This means you always have a choice and still benefit even if a particular fruit is not so good.

Funds differ based on various criteria:

Asset classes

- Equity funds invest in listed companies. They offer high potential returns, but are more volatile and are suitable for a long-term investment horizon.

- Bond funds focus on bonds, are more stable, but offer significantly lower returns – ideal for medium-term investments.

- Money market funds invest in government bonds, time deposits, or short-term corporate bonds. These investments are considered lower risk but offer less potential for returns. Ideal for a short investment horizon.

- Mixed funds combine different asset classes such as stocks and bonds and appeal to investors with a medium risk appetite.

- Those who want to specifically track trends can turn to thematic or sector funds. These include technology, healthcare, sustainability, artificial intelligence, water, and many more.

Additional criteria must be considered for thematic funds. An established fund provider with a clear focus on quality and transparency is a good sign. The same applies to fund managers with experience and a stable team. Independent rating agencies (e.g., Morningstar), seals of approval such as sustainability ratings, and awards also provide indications of a fund’s quality.

Management style

- Actively managed funds are actively managed by fund managers and pursue a specific goal. This agility is particularly advantageous in niche and thematic markets, small caps (i.e., smaller listed companies), and emerging markets. In these markets, it is important to separate good investments from bad ones based on knowledge and experience in order to generate the best possible returns for investors. One example of this is our specialized water fund. The downside is slightly higher management costs.

- Passive funds, such as ETFs or index funds, track an index (market), are significantly cheaper, and are well suited to broadly diversified, long-term investment strategies. There is no active intervention in the event of market fluctuations.

Fund Structure

- Physical funds actually own the assets (e.g., stocks). The fund holds the securities in which it invests. This means that investors participate in the real assets through the fund. This structure is recommended.

- Synthetic funds do not directly own the assets. Instead, they replicate the performance of the desired assets using financial instruments, allowing investors to participate in their performance without the assets actually being held in the fund. This creates additional risks, as investors are dependent on the solvency of the issuers. Overall, the functioning and risks for investors are often less transparent.

-> You can find out whether a fund is physical or synthetic in the fact sheet. Either in the description of the fund or in the key data. Certain online tools also allow you to filter by this criterion. On www.justetf.com, physical funds are referred to as “full” or “sampling,” while synthetic funds are referred to as ‘hybrid’ or “swap.”

Use of income

- A distributing fund regularly passes on income such as interest or dividends to you. This means you receive regular payments directly from the assets held in the fund. Distributing tranches are suitable for investors who want to receive regular income, e.g. to supplement their pension.

- A reinvesting fund retains the income in the fund and automatically reinvests it. This allows investors to benefit from the compound interest effect, as the income itself generates further income. Reinvesting funds are ideal for long-term wealth accumulation.

Online tools can help you narrow down your search. There are many websites where you can narrow down and compare funds, similar to how you search for hotels on Booking.com. One such site for passive funds with many filter options is www.justetf.com/ch/. Otherwise, experts such as Tareno will of course be happy to help you.

Which fund should I choose?

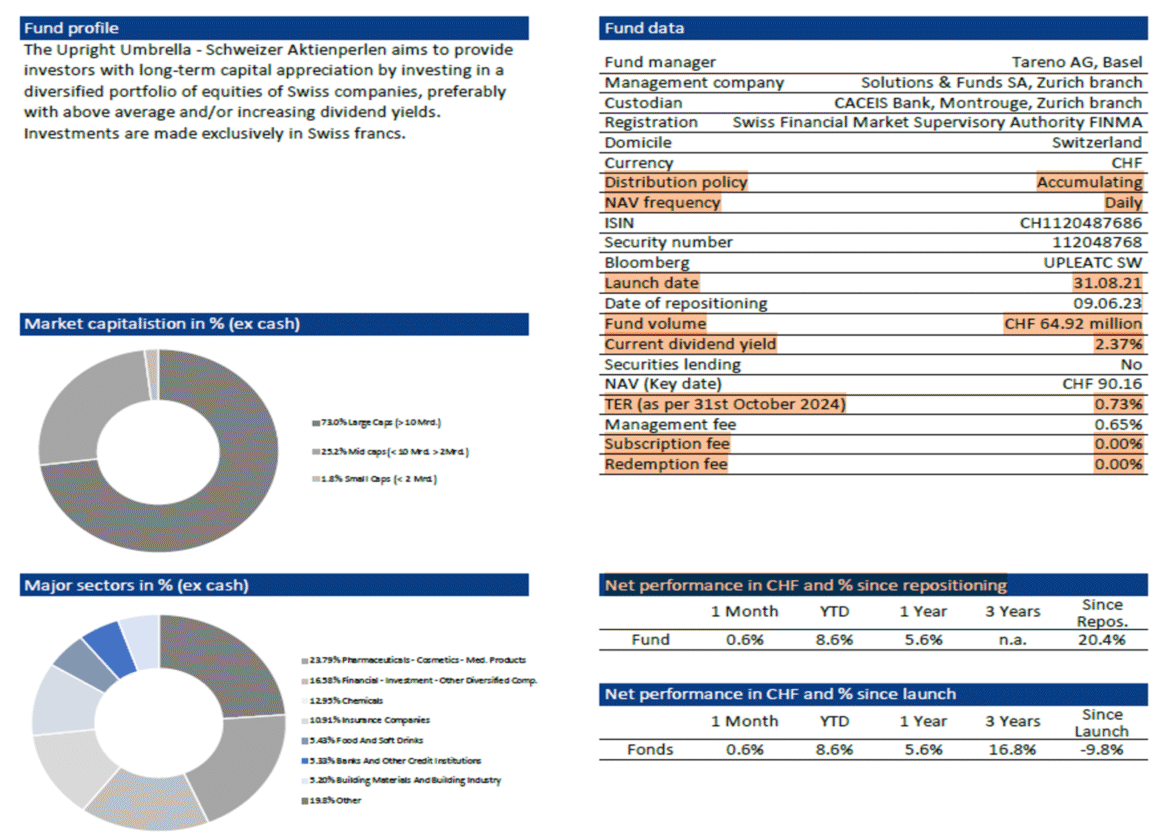

After the initial filtering and rough narrowing down, the important detailed work follows: comparing and contrasting the funds. For this, you will need the fact sheet. A fact sheet provides a compact overview and contains the most important information about a fund. All fact sheets must be freely accessible to you online and contain the following information, as listed below.

Invest in your funds

Find the fact sheets for the handful of funds you filtered earlier and highlight the most important information. Carefully compare the following key figures:

- Tradability: A fund should be tradable on a daily basis.

- Costs: The lower the costs, the more capital remains available for investment. The costs of a fund are made up of various components:

- Ongoing fund costs (TER): For passive funds such as ETFs, these are generally lower, between 0.1% and 0.5%. Active funds have higher costs, typically between 1% and 3%, and also differ depending on the fund tranche.

- One-time costs: These are sometimes charged once and come in various forms:

- Front-end load: Calculated based on the share value (my share of the total fund) when purchasing the fund. This can be up to 5%, but 0–3% is typical. For example, if I invest CHF 100 and the front-end load is 5%, only CHF 95 is actually invested in the fund. The remaining CHF 5 goes to the fund issuer to cover costs.

- Redemption fee: Very rarely charged on the share value when selling, and amounts to 0–1%. It is calculated in the same way as the front-end load, but is applied to the sale value of the product.

- External costs: These include, for example, custody, transaction, or advisory fees charged by your bank independently of the fund provider. Depending on the bank, these are charged as a percentage of the investment volume (usually between 0.1 and 0.5%) or as a flat annual fee.

-> Our tip: Pay attention to the total costs, i.e. the sum of all the costs listed above. Even small differences can have a big impact on the performance of your fund in the long term. Check the fact sheet and ask your bank or asset manager to provide you with a transparent overview of all the costs involved.

- Performance: A fund’s past performance can provide clues, but it is no guarantee of future performance.

- Fund size and duration: Check how large a fund is and how long it has been on the market. A fund that is too small carries the risk of possible dissolution, while a large fund with a long duration can be an indication of stability.

- Right fund tranche: Many funds are available in different tranches, i.e., variants of the same fund. They differ, for example, in whether income is distributed or reinvested, whether they are aimed at private or institutional investors, in the currency, or in currency hedging.

Conclusion and help: What should I do if I have questions?

Choosing the right fund can be complex. As you have seen, there are many factors to consider: from your objectives and costs to the right tranche. If you are unsure or would like a second opinion, please feel free to contact us. Together, we will find the investment solution that suits you and your goals.

Learn more about us

Investment advice

Tareno Funds