Tareno View October 2025

Published: 09.10.2025

A promising start to the fourth quarter

The global economy is once again proving its resilience, despite high US tariffs and political uncertainty. As the Fed resumes its easing course, corporate profits are receiving an additional tailwind. The signs are therefore good that share prices will continue to rise. There are still many stocks worth buying, for example in the healthcare sector, where structural growth and solid balance sheets are convincing. The downside of monetary easing is falling yields on liquidity and bonds. This increases the importance of alternative investments in portfolios. Fortunately, there are also diverse and promising investment opportunities here, as you can read in the last part of our Tareno View.

Macroeconomic environment

The Teflon boom

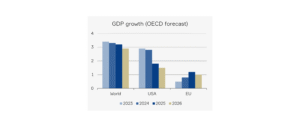

Despite all the adversities of recent years (real estate crisis in China, war in Ukraine, wave of inflation, record rise in interest rates, concerns about sovereign debt), the global economy is growing steadily at around 3% per year. Although the tariff shock is also leaving its mark, it can hardly cause the global economy to falter. Countries particularly affected, such as Switzerland, are also proving resilient and should avoid a recession even if the tariff rate of 39% remains unchanged.

On September 17, the US Federal Reserve lowered the key interest rate by 0.25 percentage points in anticipation of a possible stronger economic slowdown. At the same time, it signaled further interest rate cuts this year and next. The leading central bank has thus given the green light for a continuation of the global cycle of interest rate cuts.

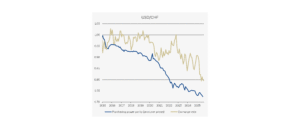

The European Central Bank and the Swiss National Bank are likely to have ended their cycle of interest rate cuts for the time being. With the expected further cuts by the US Federal Reserve and the resulting melting away of the interest rate advantage, the US dollar is likely to continue the depreciation that began at the start of the year.

A look at the purchasing power parity shows that the US dollar is still overvalued despite the recent devaluation. In view of the increasing loss of confidence, a valuation premium against the Swiss franc does not appear justified and a structural weakening of the USD is likely.

Market commentary

Good prospects

Despite customs uncertainty, global profits continue to grow robustly, led by the US technology leaders. These are benefiting from the unbroken tailwind of artificial intelligence. As AI investments are expected to continue to rise significantly in the coming year, AI stocks are likely to remain the driving force on the stock market, with positive spillover effects along the entire value chain.

For the coming year, we expect earnings growth to be more broadly supported by additional sectors. Interest rate-sensitive sectors in particular should regain momentum after a long dry spell. In view of the historically high valuation differences, we believe it makes sense to review the sector allocation. We prefer a diversified allocation to the cluster risks of many indices.

The combination of monetary easing, robust earnings growth and tailwinds from artificial intelligence should ensure that sentiment on the stock markets remains positive.

In addition to the intact fundamental data, market sentiment is also encouraging. A constructive debate about valuations is taking place across the board and positioning data shows that there is still plenty of liquidity on the sidelines that can support the markets in the event of setbacks.

Investment policy

Looking for alternatives

Although we are convinced of the potential of artificial intelligence and the earnings prospects in the technology sector, there are reasons to be cautious. Current valuations in the technology sector are high compared to the long-term averages and the overall market. After the recent strong performance, a consolidation would not be surprising in our view. In our portfolios with high technology weightings, we have therefore realized partial gains and reinvested in the healthcare sector in order to maintain a healthy balance between growth and stability.

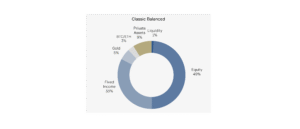

As the cycle of interest rate cuts continues, the real yields on cash holdings and bonds will also fall. In view of the high levels of government debt in many places, real yields are expected to remain low, possibly accompanied by government intervention (keyword: financial repression). Long-term investors should therefore think about their strategic allocation. We see clear added value in the addition of alternative investments as a replacement for excess liquidity and bonds, as this can significantly improve the resilience and return prospects of the portfolio. We consider gold, cryptocurrencies and private market investments to be the most convincing. Since the last Tareno View, we have increased the proportion of alternative investments in the portfolio by purchasing an Ethereum ETP and a private market fund at the expense of liquidity and bonds.

Non-US investors often ask themselves whether they should hedge the USD risk or not. From a very long-term perspective, this does not make a significant difference, as the hedging costs tend to offset the loss in value over time. However, this year and last year show impressively that the question of hedging can have a significant impact on performance in the short term.

In our view, weighing up whether to hedge the currency risk in a portfolio does not have to be a binary decision. Instead of only considering hedging the USD completely or not at all, we believe it makes more sense to neutralize part of the currency risk. We currently hedge between 40% and 50% of the USD exposure in our CHF and EUR portfolios.

Imprint

Tareno AG, Gartenstrasse 56, CH-4052 Basel, +41 61 282 28 00

Tareno AG, Claridenstrasse 34, CH-8002 Zurich, +41 44 283 28 00

info@tareno.ch

www.tareno.ch

Responsible

Simon Lutz

Chief Investment Officer

s.lutz@tareno.ch

Disclaimer

The statements and information in this publication have been compiled by Tareno AG to the best of its knowledge, in part from external (publicly accessible) sources which Tareno AG considers to be reliable, for information purposes only. This publication is not the result of a financial analysis. Tareno AG and its employees are not liable for incorrect or incomplete information or for losses or lost profits resulting from the use of information and the consideration of opinions expressed. The statements and information do not constitute a solicitation or invitation, offer or recommendation to buy or sell any investment instruments or to engage in any other transactions.

Nor do they constitute a specific investment proposal or other advice on legal, tax or other issues. A positive return on an investment in the past is no guarantee of a positive return in the future. The statements, information and opinions expressed herein are current only as of the date of this document and are subject to change at any time.

Duplication or reproduction of this publication, even in part, is not permitted without the written consent of Tareno AG. The “Guidelines for Ensuring the Independence of Financial Research” of the Swiss Bankers Association do not apply.

Images: Marijke Vosmeer, IStock, Pixabay, Unsplash, Lucia Hunziker

Charts: Tareno AG